More uncertainty, less lending: how US policy affects firm financing in Europe

2 October 2025

By Anastasia Allayioti, Giada Bozzelli, Paola Di Casola, Caterina Mendicino, Ana Skoblar and Sofia Velasco

Uncertainty is a key force shaping economic conditions. This post shows that heightened uncertainty about economic policy in the United States significantly affects firm lending in the euro area. This weighs on investment and reduces the effectiveness of monetary policy.

Periods of heightened economic policy uncertainty exert significant pressure on economic outcomes. They dampen business confidence, delay investment decisions and constrain credit conditions. When firms can’t be sure how or when regulations, tariffs or other economic policies might be implemented or change, they tend to fall into “wait and see” mode. While waiting for greater clarity, firms react to heightened uncertainty about economic policy by postponing investment decisions, while banks contract credit supply to manage potential risks.

This post takes a closer look at how economic policy uncertainty affects euro area corporate lending and the effectiveness of monetary policy in the euro area. We find that increased uncertainty about economic policies – stemming, among other things, from trade policy developments in the United States – spills over into the euro area, by reducing lending via both loan demand and loan supply. Consequently, high levels of uncertainty also make policy rate cuts less effective.

A rising ride of uncertainty

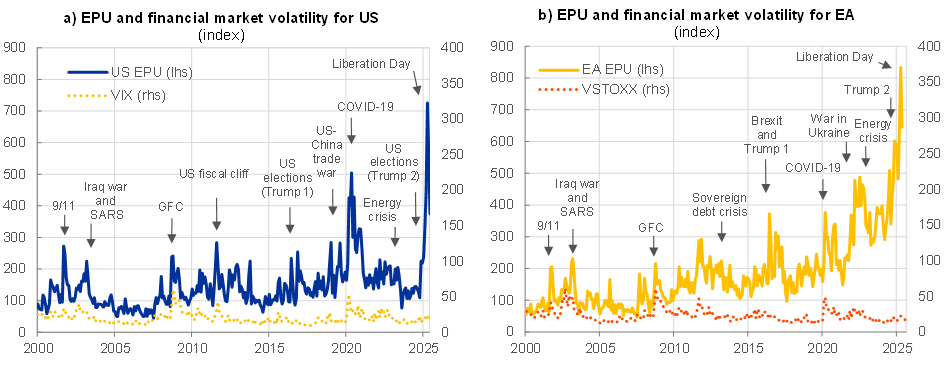

The Economic Policy Uncertainty Index, which measures the frequency of use of policy-related terms in major newspapers, has reached record highs in recent years.[1] Events like Brexit, the COVID-19 pandemic and the war in Ukraine have each contributed to these surges in uncertainty. More recent events are adding further volatility. Geopolitical risk and uncertainties surrounding US trade policy have led to peak levels in economic policy uncertainty (EPU), both in the United States and in the euro area (Chart 1). Meanwhile, financial market volatility has remained low.[2] Historically, episodes of high economic policy uncertainty have coincided with more volatile financial markets. However, recent data shows a divergence: economic policy uncertainty spikes while market volatility stays subdued. This has prompted us to examine whether policy uncertainty alone, without financial market turbulence, disrupts lending and investment.

Chart 1

Economic policy uncertainty (EPU) and financial market volatility

Sources: Baker, Bloom and Davis (2016), Bloomberg and ECB calculations

Notes: The US EPU and EA EPU are estimated by Baker, Bloom and Davis (2016). The EA EPU is constructed as a GDP weighted average of country-level indices.

The latest observation is for August 2025 (monthly observations).

Policy uncertainty affects lending

Our analysis shows that economic policy uncertainty, no matter if caused at home in Europe or in the United States, can significantly impact corporate lending in the euro area. Spikes in uncertainty stemming from monetary, fiscal, financial or trade policy developments in the United States spill over into the euro area via financial and trade linkages. To quantify the associated effects, we use a structural Bayesian Vector Autoregression (VAR) model. This allows us to assess how unexpected changes in US economic policy – which are exogenous to the euro area – affect lending conditions in the euro area via multiple transmission channels.[3]

Using aggregate euro area data since 2003, our results show that a one standard deviation shock in the model leads to a slowdown in loan growth, with effects building over time and peaking at about 0.5 percentage points roughly two years after the initial shock (Chart 2, panel a). So, when unexpected changes happen, banks give out fewer and fewer loans.[4]

The impact of uncertainty is even more severe during episodes of high financial market volatility. When volatility goes up, investors demand higher compensation for risk – known as a “volatility risk premium” – further amplifying the negative effect of policy uncertainty. Our estimates suggest that this amplifying effect would add significantly to the contraction in lending, by about 0.3 percentage points (Chart 2, panel a). Together, these results reinforce the finding that policy uncertainty – especially when coupled with financial stress – can hinder the flow of credit and slow down economic activity just when stimulus is most needed.

Chart 2

Economic policy uncertainty, lending to firms and monetary policy effectiveness

Sources: Baker, Bloom and Davis (2016), ECB and ECB calculations.

Notes: Panel a): The results are based on data on aggregate EA bank lending to firms since 2003 and a macro-financial structural Bayesian quantile model identified through recursive ordering. The panel illustrates the impact of a one standard deviation shock to US EPU on the peak effect of the shock on euro area loans to non-financial corporations. High financial market volatility indicates levels in the top quintile of realisations of the VSTOXX. Panel b): The results are based on bank-level data since 2007 for a representative sample of 80 euro area banks, and a structural Bayesian VAR model identified through a recursive ordering approach. The panel illustrates the effect of a one standard deviation shock to US EPU on peak differences of the shock on bank loan volumes (annual growth rates) across banks with high and low reserves over assets and non-performing loan ratios. High and low categories refer to the top 40% and bottom 40% of the corresponding indicator. Panel c): The results are based on euro area firm-level data since 2013. The panel illustrates the percentage difference in the impact of a policy rate surprise on firms’ investment following an increase in US EPU faced by euro area firms of one standard deviation from its median. The results are based on panel regression using firm-level data, with time and country fixed effects, using monetary policy surprises from Altavilla et al. (2019) interacted with the uncertainty measure.

The latest observations are for the first quarter of 2025 (panel a), February 2025 (panel b) and 2024 Q4 (panel c).

Uncertainty and bank credit supply

Recent empirical studies demonstrate that economic policy uncertainty does not go unnoticed by banks, but directly affects their lending behaviour.[5] Our study confirms these results: specifically, we find that when uncertainty about US economic policy rises, euro area banks tend to tighten credit conditions. The analysis is based on granular loan data from the Anacredit database. Loan-level evidence confirms that uncertainty is not just a concern for firms. It directly shapes how banks lend, which is consistent with survey evidence from both the euro area and the United States indicating worsening risk perception and lower risk tolerance by banks.[6]

Using detailed data on new bank loans to firms, we find that higher US EPU leads euro area banks to reduce credit supply, even after accounting for firm-specific demand and ongoing lending relationships. The effect is particularly strong for banks that are more exposed to the US dollar. These banks reduce their lending supply to euro area firms by more than less exposed banks. Banks that are more exposed to uncertainty about US economic policy also increase interest rates on new loans and reduce their maturity. These effects are more pronounced for firms that trade more heavily with the United States.

Other bank characteristics also matter. Credit institutions with lower liquidity, or higher shares of non-performing loans react more sharply (Chart 2, panel b). Using data since 2007 for a sample of 80 euro area banks, we find that an increase in US-driven EPU generally reduces the provision of bank-level credit to firms. That is in line with the aggregate results (Chart 2, panel a). However, a one standard deviation shock reduces loan growth by about 1 percentage point more for low-liquidity banks compared with their higher-liquidity peers. This divergence persists for up to two years. Likewise, banks with more non-performing loans experience a similarly steeper decline in their lending activity in response to an uncertainty shock. So, while banks tend to lend less in times of stress, how much less depends on specific bank balance sheet characteristics.

Implications for monetary policy

So, why does this matter for central banks? Heightened economic policy uncertainty, which stems, for example, from sudden shifts in US trade or fiscal policy, weakens the monetary policy transmission channel. During periods of heightened economic policy uncertainty, the effectiveness of monetary policy rate cuts in stimulating the economy declines significantly.[7] For investment, the impact of a 100 basis points cut in the short term rate is about 20 percent lower (Chart 2, panel c). This effect is especially pronounced among investment-intensive firms.[8] Hence, in periods of elevated uncertainty, central banks may need to respond more forcefully to achieve the same intended impact as they would under low uncertainty.

Looking ahead

As this post shows, economic policy uncertainty can significantly influence credit dynamics, business investment and the effectiveness of monetary policy in the euro area. When uncertainty rises, firms tend to delay or scale back investment. This effect is especially visible among firms operating in sectors that are more exposed to the United States. At the same time, banks – particularly those with high US exposure, limited liquidity or higher levels of non-performing loans – tighten credit conditions. And this reduces lending. As a result, policy uncertainty, even when it originates in the United States, can weaken the effectiveness of monetary policy in the euro area.

The views expressed in each blog entry are those of the author(s) and do not necessarily represent the views of the European Central Bank and the Eurosystem.

Check out The ECB Blog and subscribe for future posts.

For topics relating to banking supervision, why not have a look at The Supervision Blog?

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.